The video games industry, estimated to be worth $200 billion, is experiencing its most significant slowdown in three decades as the massive expansion propelled by mobile gaming and the newest console generation hits a plateau.

Sales of hardware are decelerating, as exemplified by Sony’s recent reduction in its PlayStation 5 sales projections. Additionally, spending on mobile games diminished last year by 2%, amounting to $107.3bn, as per Data.ai, which predicts a modest increase in growth by 2024.

This perceived industry-wide issue sharply contrasts the growth seen during the COVID-19 pandemic, when many consumers confined at home allocated their extra time and money to games. The original PlayStation launched the digital entertainment industry into a prosperous phase in the middle of the 1990s, and Apple’s iPhone gave it an additional boost.

Many industry insiders anticipated a swift recovery following the 2022 post-pandemic downturn in the gaming industry, but the growth experienced last year fell short of expectations.

Recent quarterly results from leading publishers like Electronic Arts and Take Two have disappointed investors. Concurrently, game developers, after already eliminating around 10,000 positions in 2023, have had to make further significant job cuts this year.

Challenges and Strategies in the Console Market

The stagnation in sales of new gaming devices is causing concern for market expansion. The surge from the release of the latest PlayStation and Xbox consoles in 2020 is fading, and the worldwide slump in smartphone sales is leading to fewer new gamers in what has recently become the most profitable segment of the industry.

Sony’s gaming unit head, Hiroki Totoki, announced that the PlayStation 5, which crossed 50 million units in December, is “transitioning into the latter part of the console cycle, predicting a steady decrease in unit sales starting from the next fiscal year.”

Sony’s severe PS5 price cuts in 2023 have already resulted in what Totoki described as a “significant” fall in the company’s gaming operating profits. He cautioned that Sony “has no plans to launch any new major existing franchise titles” in the fiscal year beginning in April, eliminating potential revenue from blockbuster games like Spider-Man or God of War.

Microsoft, trailing far behind Nintendo and Sony with its Xbox, revealed plans this week to sell more of its own games on competitor consoles, aiming to explore new growth avenues in a market that is becoming increasingly saturated, especially after its $75 billion acquisition of Activision Blizzard last year.

The expected launch of a new Nintendo console later this year might further hasten the decline in PlayStation and Xbox sales, as gamers start saving for the upcoming release.

The gaming industry is grappling with a console-based challenge: Xbox sales are flagging, the PlayStation 5 has reached its zenith, but only through substantial price reductions, and the gaming community is eagerly awaiting the arrival of the Switch 2.0. The performance of consoles underscores that they are not a sustainable growth strategy for the gaming sector, as their sales reach a definitive limit.

Gaming Industry Growth Challenges and the Prospect of New Market Strategies

Microsoft Gaming’s head, Phil Spencer, referenced a recent study by technology author and investor Matthew Ball. The report revealed that the gaming industry experienced less than 1% growth last year. This growth rate is slower than inflation and most GDP growth, indicating that the gaming industry’s significance declined last year compared to other entertainment sectors.

The sector’s primary opportunity lies in discovering new growth avenues among players who cannot afford a $500 console or a $70 game. The industry should focus on the question, “How can we bring games to individuals who aren’t currently playing and cannot afford to play?” Lowering game prices can be a risky move. Free-to-play online games like Fortnite and Roblox have become immensely popular, taking up the time players used to spend on more expensive $70 games. Also, the popularity of multiplayer games like Call of Duty makes it even more difficult for new games to gain traction. The market is flooded with thousands of new games every month, and very few find success. Therefore, launching a new product in this market is a significant challenge. The escalating expenses of producing major video games have significantly heightened the risks. With budgets exceeding $100 million, even a few failed projects can pose serious commercial problems for large companies.

This has triggered a trend reminiscent of Hollywood, where companies like Sony, Microsoft, and Electronic Arts rely heavily on reviving well-known franchises. Simultaneously, major entertainment entities are showing a renewed interest in the gaming industry, introducing new competition in a market that’s witnessing a decline.

Disney recently invested $1.5 billion in Epic Games, the creator of Fortnite, to establish what the studio’s chief, Bob Iger, described as “a vast Disney universe for gaming and play”. Concurrently, Netflix is broadening its offerings in the gaming domain. Disney leverages its intellectual property from movies and television into games, similar to how it is incorporated into their parks. This strategy follows the revelation of demographic trends. According to these patterns, younger audiences divide their time equally between gaming and traditional forms of entertainment like TV and movies and this is something the gaming industry needs to take into serious consideration.

Sony’s Struggles with PlayStation 5 and the Challenges of High Development Costs

While the release of the exclusive title, Final Fantasy VII Rebirth, should have marked a period of triumph for Sony Group Corp.’s PlayStation 5, the reality appears quite different. Despite the game receiving critical acclaim, the company seems to be facing challenges. Sony unexpectedly announced in its recent earnings report that the PlayStation 5, now three years old, has essentially hit its peak. The company anticipates a gradual decrease in hardware sales beginning next year as the console enters its later stages. As a result, Sony is reducing its global workforce in the gaming division by approximately 900 employees and discontinuing several games in development.

The company acknowledged that the PS5 won’t have any new major first-party titles until at least April 2025, a disappointment for gamers. Despite the PS5 still feeling new due to the pandemic’s distortion of time, it’s already nearing its peak.

Sony, like many others in the industry, is battling issues of inflated development cycles and budgets. The Final Fantasy VII remake serves as a prime example. The original game, launched in 1997, had a budget of around $40 million and took just over a year to complete. The remake, however, has grown so massive that it’s divided into three separate games. The first chapter, released four years ago, reportedly cost $140 million.

This level of spending is not sustainable. Sony’s President and CFO, Hiroki Totoki, has indicated a desire to control costs. He recently assumed interim direct control over the gaming division, consolidating power back in Japan after years of English leadership under Jim Ryan.

Totoki’s impressions appear to be unfavourable based on his recent comments. He stated that first-party studios need to enhance their understanding of profit generation and expense management. Coupled with the layoffs and closure of Sony’s London studio, the message is evident: Sony is not getting an adequate return on its investment, especially considering that one of its most prominent studios has only produced one new game in the past eight years.

Extended Game Development Cycles and the Shift in Exclusivity Policies

A similar scenario is unfolding at Nintendo. Numerous reports suggest that the Switch’s successor, initially expected to be released this year, won’t make its debut until at least March 2025. Nintendo is giving developers more time to produce software, according to the Nikkei newspaper. Around 80% of its software revenue originates from its in-house-developed games.

The timeline for creating high-quality games has been significantly extended. A decade ago, it was common for an AAA game to take around three years to complete. Now, it’s not unusual for companies to require double that time. A six-year gap occurred between the release of Legend of Zelda: Breath of the Wild and its sequel, Tears of the Kingdom. The latest mainstream 3D Mario game launched in 2017, and there hasn’t been a new Mario Kart for ten years. The anticipated expanded specifications of the Switch’s successor are expected to further lengthen these development cycles.

Microsoft is dealing with similar challenges, but it’s adopting an unconventional solution: it’s opting to launch games that were originally exclusive to Xbox, such as the highly praised Hi-Fi Rush, on Sony and Nintendo’s platforms. This decision has upset dedicated Xbox fans, but Microsoft appears to be distancing itself from the concept of exclusives. It has committed to making Call of Duty, which it obtained through its acquisition of Activision Blizzard, accessible on competing systems.

It’s easy to see why high production costs are an issue. While publishers typically don’t disclose budget specifics, leaks suggest Sony’s Insomniac studio’s Spider-Man 2 had a budget of around $300 million. Although this game was successful, many others, like Square Enix’s Forspoken with its AAA budget, did not fare as well. It’s sales were described as “lacklustre” by the company. Similarly, Warner Bros. Discovery Inc.’s Suicide Squad: Kill the Justice League, in development since 2017, underperformed, according to company executives.

Attempts to justify these growing budgets with increased game prices have been met with resistance from gamers, who expect prices to eventually fall. Capcom’s President, Haruhiro Tsujimoto, expressed frustration with this last year, noting that game prices have barely increased despite a hundredfold rise in production budgets since the mid-1980s.

Additionally, high budgets lead to risk-averse strategies among companies, resulting in a lack of diverse software and many games feeling similar. Many studios aim to create a “live-service” game that can be continually monetized, but few succeed. Gamers often turn to unexpected titles like 2023’s Baldur’s Gate 3 or the recent indie hit Palworld, adding uncertainty to what kind of games developers should create.

The recent wave of layoffs in the industry reflects the fluctuating needs for resources in game development. While hundreds of people may be needed during crunch periods, fewer are needed during the early prototype stages. The trend of hiring as tech firms do in an era of seemingly endless funds is proving to be unsustainable, especially when the average US game developer’s salary exceeds $100,000.

In the future, AI might help with the creation of game assets, but players are still skeptical of artificially created art. Ultimately, the gaming industry is in a period of adjustment and still seeking the ideal business model. Both developers and gamers should brace themselves for potential instability in the years to come.

A Trader’s Insight

Today we will be talking about USD strengths in recent years and the possibility of a correction in USD given the recent Fed announcement.

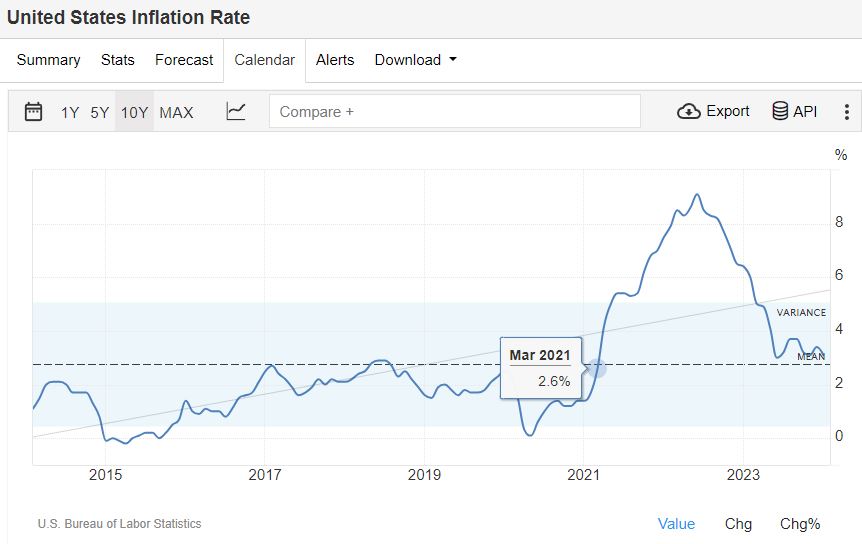

Firstly, we have to look at the correlation between the US inflation rate and the US dollar, as shown in the above 2 charts. The US inflation rate starts trending upward, breaking off its 10-year mean at around Mar 2021, which corresponds with USD strengthening in June 2021.

And continuing with the inflation rate, which peaked at around June 2022 and started trending down since then, we can see a similar movement by the USD, where it started trending downwards at around September 2022.

What we have observed is that inflation tends to be the leading indicator for US dollar movement, with the USD movement lagging around 2-4 months. As we can see here, inflation has since moved towards its 10-year mean. I personally expect the inflation to be moving sideways close to the 10-year mean; hence, I also expect the USD to be trending sideways despite the recent Fed announcement on the possibility of a rate cut.

In conclusion, I think that USD has already priced in the possibility of a Fed rate cut, and the movement of the inflation rate would be my focus in deciding the strength/weakness of USD. Although further USD corrections are expected in the short term, I believe that the US dollar will be trading sideways against the major currencies unless there are sudden changes to the US inflation rate.

Terry Loh